There is a moment that keeps showing up in my conversations with CIOs, and I have seen it often enough now to recognize it before it arrives. The leader walks me through everything the organization has done over the last eighteen months, the copilots rolled out to every engineer, the training programs launched, the pilots greenlit, the AI council stood up, the board deck that finally looks the way the board wanted it to look. The progress is real, and they describe it with conviction, because the metrics moved and the engineers are genuinely faster.

And then there is a pause. Some version of the same sentence follows it every time. “We have done all of this, and we are still not where we need to be.” That pause is not confusion. It is recognition. They already know what is missing. They just do not have language for it yet. This article is that language.

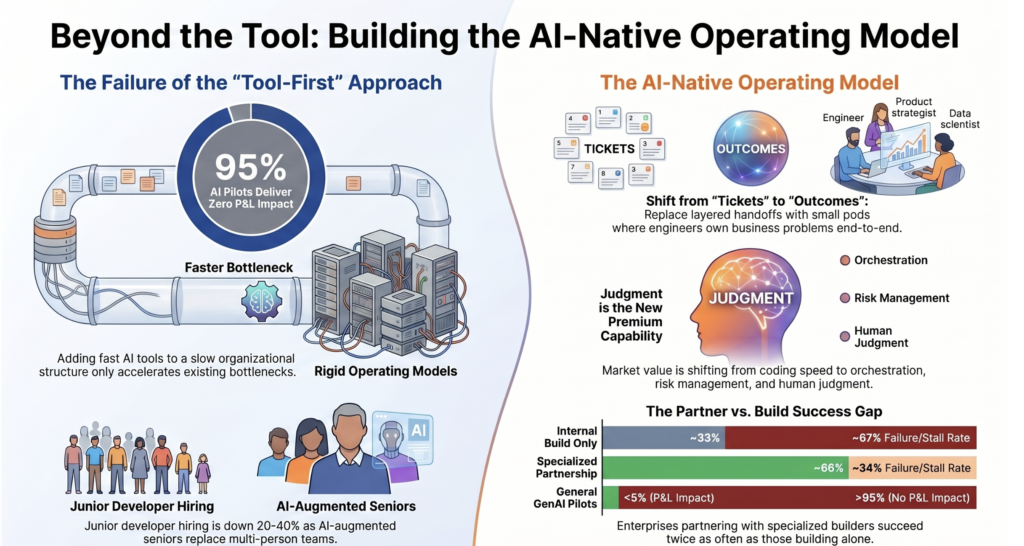

The tools were never the hard part

Here is the uncomfortable truth the pause is pointing at. The tools were never the thing that was going to move you. MIT’s 2025 study of three hundred enterprise AI deployments found that ninety-five percent of generative AI pilots delivered no measurable impact on the P&L, and the failures had almost nothing to do with model quality and almost everything to do with the operating model the tools were dropped into. Gartner found the same pattern from another angle, with at least half of enterprise GenAI projects abandoned after the proof of concept.

You can buy every license on the market and still sit exactly where you started, because a faster engineer inside a slow operating model produces a slightly faster version of the same bottleneck. The capability accelerated. The organization around it did not. That gap, between what the tools can now do and what the organization is built to absorb, is where most enterprises are quietly stuck right now.

What AI-native actually looks like

So let me be specific about the destination, because vague aspiration is the enemy here. In the first article in this series I described the rise of the product-minded engineer, and in the second what it actually takes to build a product-minded engineering organization. Both named the problem. Neither said the quiet part, which is this. An AI-native engineering organization is not your current organization with AI added on top. It is a different operating model, and it has a knowable shape.

Small outcome-based pods in place of layered handoffs between product and engineering. Engineers who own a business problem end to end rather than a ticket. Validation infrastructure that scales with how fast code is now generated, which matters more than ever when AI already writes close to half of all new code in many shops and Deloitte projects thirty to thirty-five percent productivity gains across the development lifecycle. Governance that states clearly what an AI system is allowed to decide on its own and what still requires a human. Leadership that measures the speed of the system rather than the velocity of any one person. That is what Stage 4 looks like as an operating state you can staff and measure.

The talent math is already moving

The numbers underneath this are shifting faster than most workforce plans assume. Employment for software developers aged twenty-two to twenty-five has fallen close to twenty percent since late 2022, and entry-level engineering postings are down somewhere between a quarter and forty percent from their peak, because one senior engineer with AI now ships what used to take that senior plus two juniors.

At the same time, the capability that has become scarce and expensive is not coding speed. It is judgment. Workers with AI skills already command meaningfully higher pay, and the roles tied to orchestration and governance, the people who can define the boundaries of autonomous action and explain AI risk to a compliance officer whose signature decides whether a system reaches production, carry the steepest premiums in the market. This is the capability almost no training program develops well, because it cannot be taught outside the context of real systems with real stakes. The org chart you need in 2027 is not a smaller version of today’s. It is a different shape, weighted toward judgment at the edges and thin in the middle where coordination used to live.

The real decision is build or partner

Which brings the CIO to the decision that actually matters, and it is not a technology decision. It is whether to build this new operating model from scratch while running a technology organization at full scale, or to navigate the transition with a system that already knows the path. The same MIT research that found ninety-five percent of pilots stalling also found something the headlines skipped. Enterprises that partnered with specialized external builders succeeded roughly two-thirds of the time, while internal builds succeeded only about a third as often. The pattern matches everything I see inside enterprises. The organizations that try to invent the operating model alone spend their eighteen-month window discovering what others already know, and the window does not wait for them.

What Arula actually is

This is the work I built Arula to do, and I want to be precise about it, because the category confusion is real. Arula is the operating infrastructure for the transition this series has been describing, and it runs on three practices that work as one system.

Forge takes the judgment that lives inside an organization, the pattern recognition a senior leader built over twenty years that was never codified because there was never a mechanism to codify it, and encodes it into an operating agent inside a three-week sprint. Foundry delivers through small outcome-based pods that become the working proof of the operating model the client needs to build internally, and the question clients ask when they watch a Foundry squad ship is always the same, which is why their own organization is not structured this way. Prowess certifies the judgment layer itself, the governance and orchestration capability that lets AI systems operate at scale inside a regulated enterprise, the exact capability the market is now paying a premium for. Encode the knowledge, demonstrate the model, build the human capability that makes it stick. Three parts, one system.

The question that separates the CIOs who make it

The leaders I have watched make this transition cleanly share one trait that predicts more than budget, more than talent, more than the technology stack they chose. They stopped asking how to add AI to what already exists, and started asking what the organization would look like if it were built from scratch around what AI now makes possible. That question produces a different answer for every enterprise, different team structures, different hiring criteria, different governance models, different definitions of what ownership means. The direction is always the same. Smaller teams, more direct ownership, less coordination overhead, faster loops between an engineering decision and a business outcome.

The eighteen-month window I named in the first article is real, and it is moving. The organizations beginning the Stage 2 to Stage 3 transition now will hold a structural hiring and delivery advantage by mid-2027, and the ones still debating strategy will be competing for talent and outcomes in a market that has already moved past them. The answer was never a tool. It was always the operating model designed around what the tools make possible.

So here is the question worth sitting with this week, the one that separates the CIOs who navigate this from the ones who get navigated by it. If you rebuilt your engineering organization from scratch tomorrow around what AI can do today, how much of what you have would you keep? Sit with your honest answer. Then start.

Keep Growing.

Gunjan

Sources

MIT, State of AI in Business 2025 (GenAI Divide, 95% of pilots, build-vs-partner success rates). Gartner, GenAI project abandonment after PoC. Deloitte 2026 Software Industry Outlook (30–35% productivity gains). Stanford Digital Economy Lab and CIO Dive (entry-level developer employment decline). AI skills wage and orchestration/governance premium data, 2026.

Editor’s note — suggested visual

Insert one diagram around the “what AI-native actually looks like” section: a four-stage maturity bar (Stage 1 pilots → Stage 4 operating state) with the five markers of Stage 4 listed beneath it (outcome pods, end-to-end ownership, validation at generation speed, decision-boundary governance, system-speed metrics). It lets a CIO locate themselves at a glance and makes the piece far more shareable.